Kuflink has been around as a bridging finance lender since 2011, formerly being known as Alpha Bridging. In 2016, the company rebranded as Kuflink and they began giving peer-to-peer lenders access to their loan book.

Since becoming a peer-to-peer, Kuflink has loaned over £48m. They claim that no investor has lost any money on the platform to date.

How's it working out for me, and should you get involved too? My Kufflink review will tell you everything you need to know…

Remember: peer-to-peer lending involves risk. I've not hammered home the risk point in this article because it's covered in my main peer-to-peer lending article. Make sure you read that before investing if you're not familiar with how peer-to-peer lending works and what the risks are.

What makes Kuflink unique?

While some other platforms now do it, I believe Kuflink were the first to co-invest by taking a 5% share in each loan. Importantly, this 5% is in a first-loss position – so if anything goes wrong with a loan, they'll lose all their investment before investors lose anything.

For us as investors, this effectively reduces the loan-to-value ratio of each loan: if Kuflink loaned 70% of a property's value, our exposure will only be 65%. It's clearly not enough to protect against a major drop in value or a drastically over-optimistic valuation, but it does disincentivise Kuflink from making overly risky loans – because they'd lose out too.

(I believe this is a major problem for most platforms: they make their money when they lend, so in marginal situations their incentive is to go ahead rather than be cautious.)

What are you lending against?

All Kuflink loans are secured against property, and loan terms are 3-24 months (most around 12). I obviously like the property security, and I also like the short duration: with a maximum term of a year, there aren't any large and complex projects that will take years to build out and have more scope for something to go wrong.

Looking at the loans currently on the platform, most are either small development projects or people wanting to use a property as security for a business loan or to consolidate other debts.

Most Kuflink loans are secured by a first charge – meaning that if the borrower defaults, they can force a sale and be first in line for the proceeds. There are some second charge loans, which means there's an existing lender who's first in line to be paid back. I tend to avoid these, because I perceive them as being higher risk without a high enough return to match.

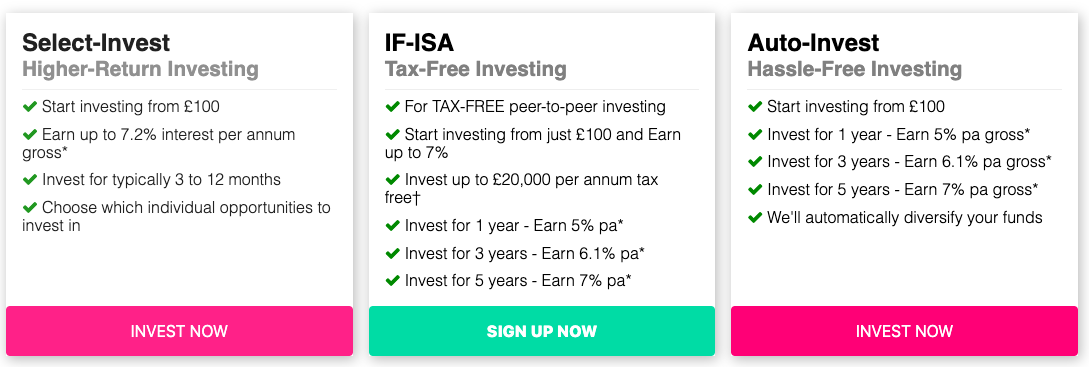

What are the investment options?

There are two options:

- Select-invest, which means you choose which specific loans you want to invest in.

- Auto-invest, which automatically spreads your investment across a pool of loans.

Kuflink also offers a peer-to-peer ISA option, although you can only use uato-invest in your ISA.

How select-invest works

This is where you get to play property investor, and decide which individual projects you want to fund.

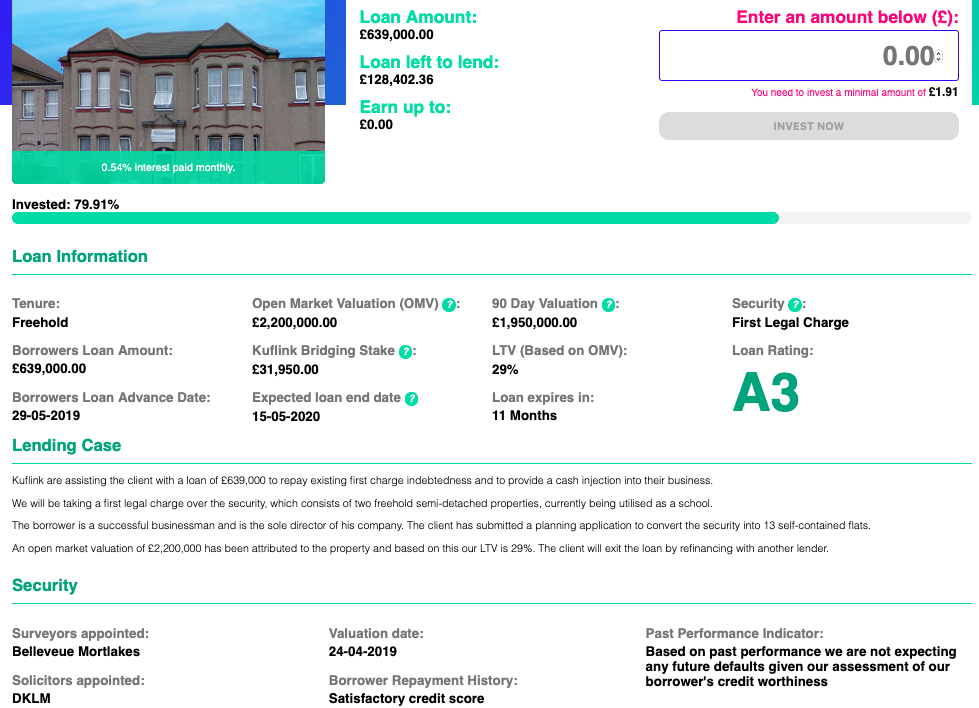

You can achieve an impressive amount of diversification between loans, because the minimum investment is extremely low (although you need to make an initial investment of at least £100 onto the platform as a whole). Per loan, you only need to invest enough to make sure you earn at least 1p in interest per month – so for a loan paying 0.57% monthly, you need to invest at least £1.76.

Loans are priced according to risk, and the loans currently live on the platform range between 6.5% and 7.2% per year.

For each loan, you see an impressive amount of detail, including:

- The valuation of the property

- The loan-to-value and loan-to-GDV (if appropriate)

- The security being taken

- Who the borrower is, and why they are borrowing

- How much investment is still available, and how much of a stake Kuflink are taking themselves

There's also a loan rating on an A1 to C3 scale, which I completely ignore: I prefer to come to my own view based on the information provided.

Something I really appreciate is that the original valuation report (from a RICS surveyor) is available, so you can dive into lots of detail if you want to. If you're only putting a few pounds into each loan this is unlikely to be a good use of your time, but if you want to put in bigger chunks it's nice to have the source materials to make your decision on rather than just Kuflink's commentary.

Then you click a couple of buttons, and boom – you're invested! If a loan isn't yet live, you can still “reserve” a share and receive interest while your funds are sitting around waiting for the loan to start (you receive this interest on the day the loan actually does start). This eliminates cash drag, so it's a nice feature.

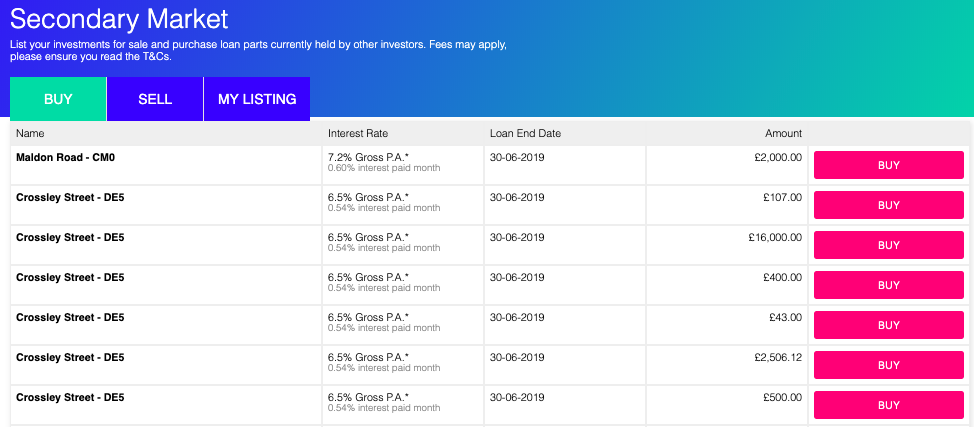

The secondary market

Kuflink has fairly recently added a secondary market, which is fantastic: it means you can exit loans early by selling your loan parts to other investors. There is a 0.25% fee for selling loans.

This means you're not necessarily tied in for the duration of the loan if you want to get your money back out, but of course this does rely on there being someone on the other side of the transaction wanting to buy. It's always safest to assume you'll be locked in for the duration, and choose loans with short terms if you don't want to keep your cash tied up for long.

You can also buy on the secondary market if you want to diversify beyond the “fresh” loans that are available for funding.

You can only sell your entire stake in a loan, not just part, and you can only buy the whole stakes that other investors have listed. A handy side-effect of this is you can get a feel for how many investors are trying to bail out of a given loan, because they show up as individual chunks rather than being aggregated into one.

You can also only buy or sell at the original interest rate that was offered, not at a premium or discount. I actually prefer this, because it keeps things simple and I don't want to mess around with bids and offers.

How auto-invest works

Auto-invest means you stick your money in, and it gets automatically split between a pool of loans.

At the time of writing, there are about 25 loans in the pool and the total value of all the loans is around £7m. You get to see top-line details of each loan, such as its value, what security has been taken, and when it's due to repay.

You can invest for either one, three or five-year fixed terms. At the time of writing, the interest rates are:

- One year: 5%

- Three years: 6.1%

- Five years: 7%

It's important to know that you can't take your money out before the end of the term: once it's in, locked away until the end of the term. (The specific loans in the pool will change as they repay and are replaced by new ones, but you can't take anything out.)

The minimum investment in the auto-invest product is £100. You receive your interest annually, on the anniversary of your investment.

As I mentioned, you can also access the auto-invest product through an IFISA, meaning tax won't take a bite out of your returns.

What I like about Kuflink

Short-dated property loans

As I mentioned earlier, I like secured loans and I like simple loans. Kuflink delivers on both counts, so I believe the returns it offers are good on a risk-adjusted basis.

Lots of information about each loan

I like having access to the original valuation report, plus lots of other information provided by Kuflink themselves.

Kuflink's 5% share in each loan

Kuflink put 5% of their own money into each loan, which keeps their interests aligned with those of investors.

Low minimum investments

The minimum £100 investment in auto-invest makes it easy to dip your toe in, and the tiny minimum in each individual self-selected loan makes it possible to get some serious diversification.

The secondary market

I have issues with commitment, so it's nice to be able to get out early – and the secondary market is extremely easy to use and understand.

How I use Kuflink

In a dramatic break with my normal laziness, I actually use the select-invest rather than auto-invest product (although I stuck £100 into auto-invest just to see how it works).

Why? The main one is that auto-invest funds are locked away for at least a year, whereas it's possible to exit select-invest loans using the secondary market. Even if the secondary market didn't exist, there would still be loans maturing regularly so it'd be quicker to unwind my position if I needed to.

That, combined with the one-year rate in auto-invest being a good 1-1.5% lower than the majority of individual loans mean it's not appealing to me – although I like the option being there, and if you used your IFISA you might come out ahead after tax despite the lower interest rate.

So: I'm actually making a modicum of effort. I've set a reminder fortnightly, so I can pop in and re-invest any portions that have been paid back to me since I last checked. For me this is a decent compromise between reducing cash drag and reducing effort, but you could of course check in more often if maximising returns was important to you.

When it comes to selecting loans, my main approach is just to diversify as much as possible rather than taking a deep dive into the detail of every loan. If there's something about a loan that puts me off I'll steer clear (normally related to the reason for borrowing rather than anything else), otherwise I'll pop a small amount in. I have more faith in maths to keep me safe than my property expertise.